Tilley's Bundling Algorithm

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

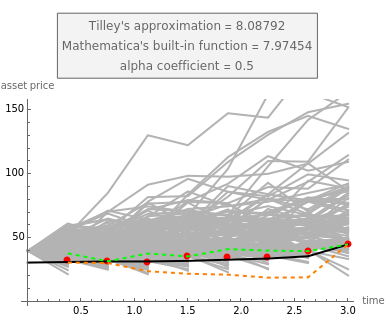

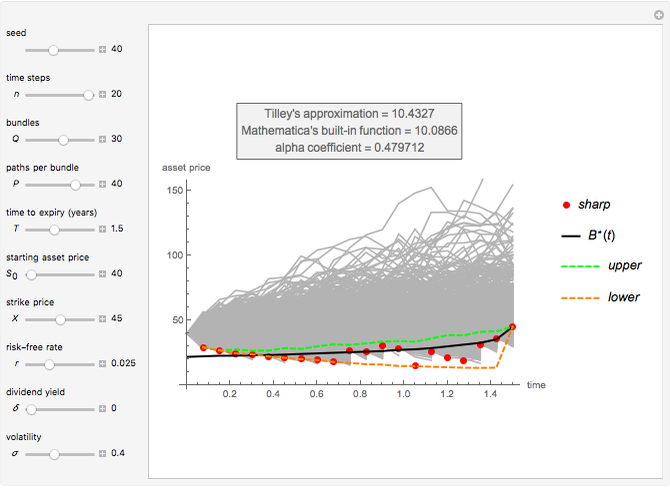

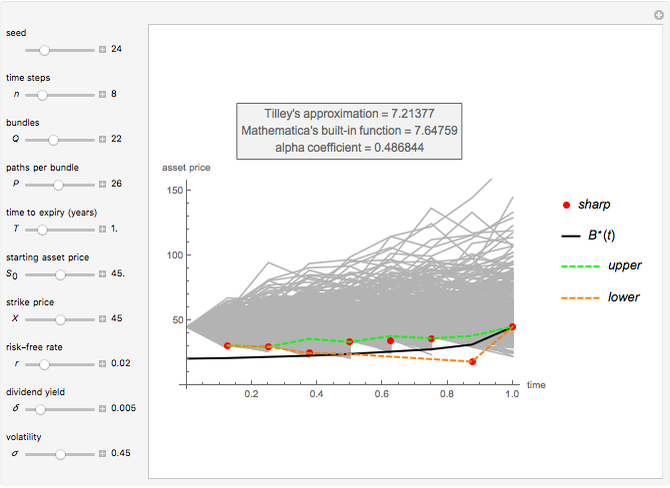

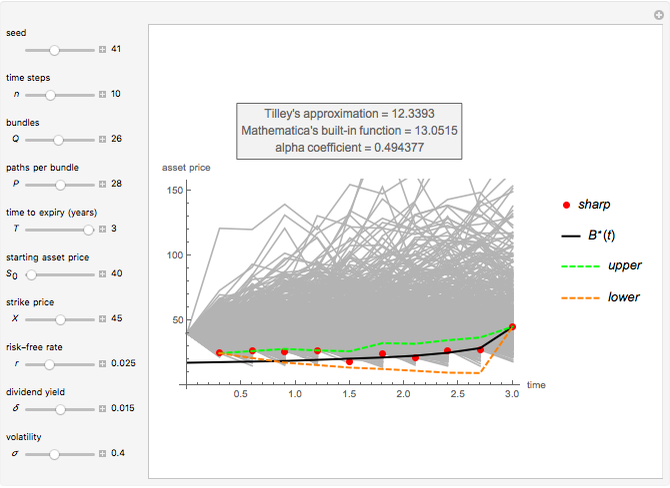

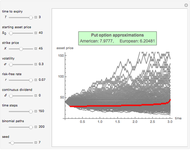

This Demonstration shows Tilley's bundling algorithm [1] that uses Monte Carlo simulation to approximate the value of an American option on a single underlying asset. The graph shows the simulated geometric Brownian motion (GBM) paths (gray lines), the "transition zone" (dashed lines), and the "sharp boundary" (red dots), which is the algorithm's approximation for the optimal exercise boundary  (black line). Whenever a GBM path falls below the "sharp boundary", the early-exercise is considered optimal and the option is instantly exercised. The early-exercise events at each time step are illustrated by the abrupt cut of those GBM paths that fall bellow the red dots. For each GMB path, the intrinsic value of the option at the time of exercise is discounted, and Monte Carlo integration helps to approximate the American put at

(black line). Whenever a GBM path falls below the "sharp boundary", the early-exercise is considered optimal and the option is instantly exercised. The early-exercise events at each time step are illustrated by the abrupt cut of those GBM paths that fall bellow the red dots. For each GMB path, the intrinsic value of the option at the time of exercise is discounted, and Monte Carlo integration helps to approximate the American put at  .

.

Contributed by: Michail Bozoudis (October 2014)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

Tilley's bundling algorithm [1] is a Monte Carlo simulation approach [2] for pricing American options. It generates pseudorandom paths that follow GBM and estimates the option’s continuation value by using backwards induction and a bundling technique. At one time step prior to maturity, paths whose stock prices are similar are grouped together to obtain an estimate of the one-period-ahead option value. Proceeding recursively from the option’s expiration date, an optimal exercise policy is obtained. The red dots represent Tilley's "sharp boundary", which is the algorithm's approximation of . The (actual) early-exercise boundary derives from Mathematica's built-in function FinancialDerivative. While the stock price moves above , the early-exercise is not optimal because the option's holding value is greater than its intrinsic value.

Tilley's "sharp boundary" lies within a "transition zone", which is determined by the dashed lines in the graph: • between the zone's upper limit and the "sharp boundary", the possibility of early-exercise is significantly low, • between the "sharp boundary" and the zone's lower limit, the possibility of early-exercise is significantly high, • outside the "transition zone", the early-exercise possibilities are considered 0% and 100%, respectively.

The "alpha" coefficient derives from  , where

, where  is the number of paths per bundle, and

is the number of paths per bundle, and  is the total number of paths.

•

is the total number of paths.

•  indicates that the simulation algorithm uses a single bundle that includes all paths,

•

indicates that the simulation algorithm uses a single bundle that includes all paths,

•  indicates that every single path is treated as a separate bundle,

•

indicates that every single path is treated as a separate bundle,

•  indicates that the number of bundles equals the number of paths per bundle. Tilley demonstrated that if

indicates that the number of bundles equals the number of paths per bundle. Tilley demonstrated that if  , the algorithm still provides good approximations for American options, even if the simulation algorithm uses the upper limit of the "transition zone" as the early-exercise boundary.

, the algorithm still provides good approximations for American options, even if the simulation algorithm uses the upper limit of the "transition zone" as the early-exercise boundary.

References

[1] J. Tilley, "Valuing American Options in a Path Simulation Model," Transactions of the Society of Actuaries, 45, 1993 pp. 83–104.

[2] M. Fu, S. Laprise, D. Madan, Y. Su, and R. Wu, "Pricing American Options: A Comparison of Monte Carlo Simulation Approaches," Journal of Computational Finance, 4, 2001 pp. 39–88.

Permanent Citation

Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis Geske-Johnson Method

Geske-Johnson Method

Michail Bozoudis Maximizing a Bermudan Put with Two Early-Exercise Temporal Points

Maximizing a Bermudan Put with Two Early-Exercise Temporal Points

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis

-

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis