Variation in the Value of Mortgage Strips

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

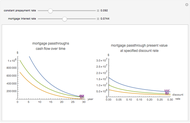

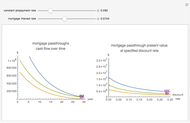

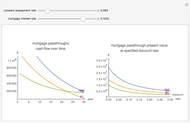

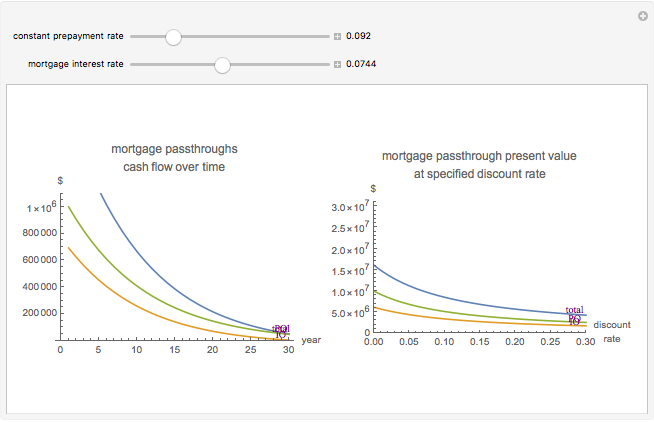

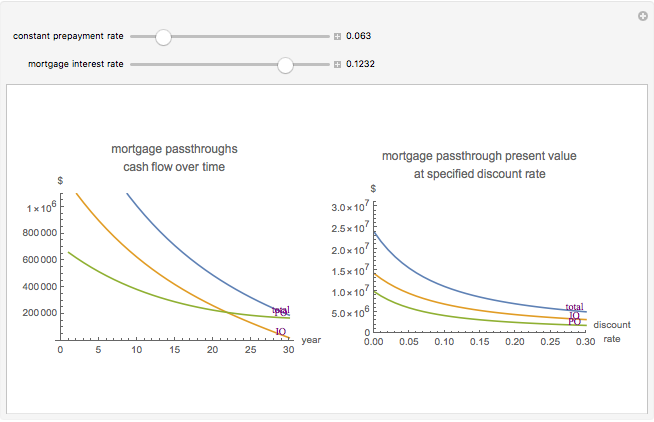

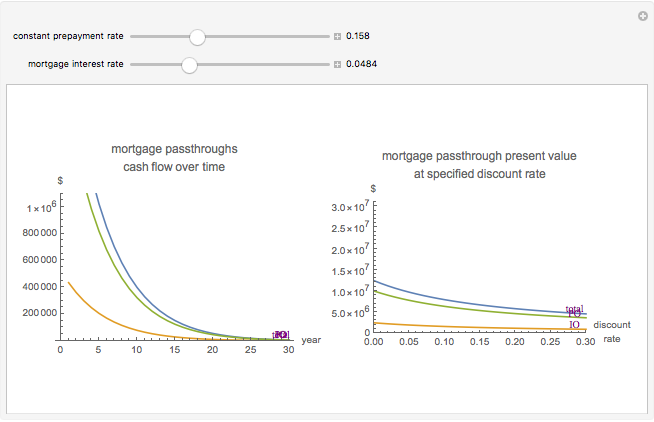

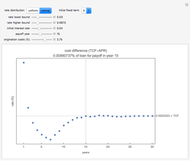

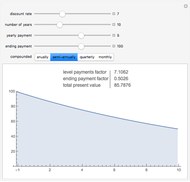

Among the most basic mortgage-backed securities are "strips". The name is derived from "Separate Trading of Registered Interest and Principal Securities", and refers to the isolation of cash flow from interest payments or principal payments on a pool of bonds. Strips can be created from almost any kind of bond or bond-like asset where cash flow can be split into interest-only (an "IO") and principal-only (a "PO") strips.

[more]

Contributed by: Michael Stern (January 2014)

Open content licensed under CC BY-NC-SA

Snapshots

Details

References

[1] C. A. Stone and A. Zissu, The Securitization Markets Handbook: Structures and Dynamics of Mortgage- and Asset-backed Securities, 2nd ed., Hoboken: Wiley, 2012.

[2] F. J. Fabozzi , A. K. Bhattacharya, and W. S. Berliner, Mortgage-Backed Securities: Products, Structuring, and Analytical Techniques., 2nd ed., Hoboken: Wiley, 2011.

Permanent Citation

"Variation in the Value of Mortgage Strips"

http://demonstrations.wolfram.com/VariationInTheValueOfMortgageStrips/

Wolfram Demonstrations Project

Published: January 21 2014

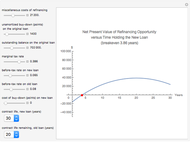

Rational Refinancing of a Residential Mortgage

Rational Refinancing of a Residential Mortgage

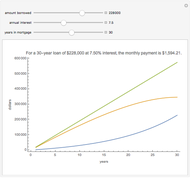

Michael Stern Mortgage Calculator

Mortgage Calculator

Ed Pegg Jr True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown and Tom Compton Options: Time Value

Options: Time Value

Peter Falloon Earned Value Management

Earned Value Management

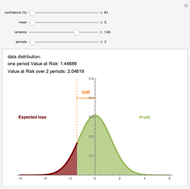

Hagen Lotze Value at Risk

Value at Risk

Gergely Nagy Present Value Calculator

Present Value Calculator

Craig Bauling Future Value Calculator

Future Value Calculator

Sarah Lichtblau Net Present Value

Net Present Value

Fiona Maclachlan Discounted Present Value

Discounted Present Value

Jason Cawley