Forecasting with Exponential Moving Averages

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

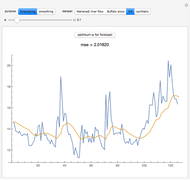

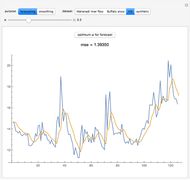

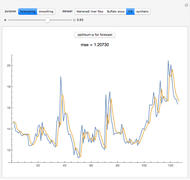

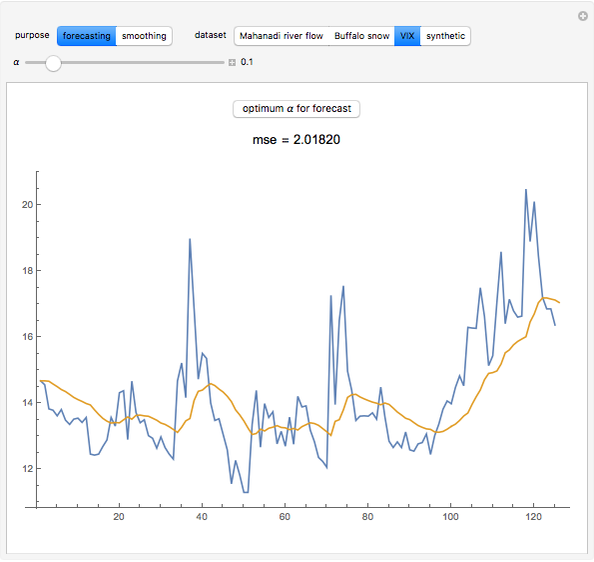

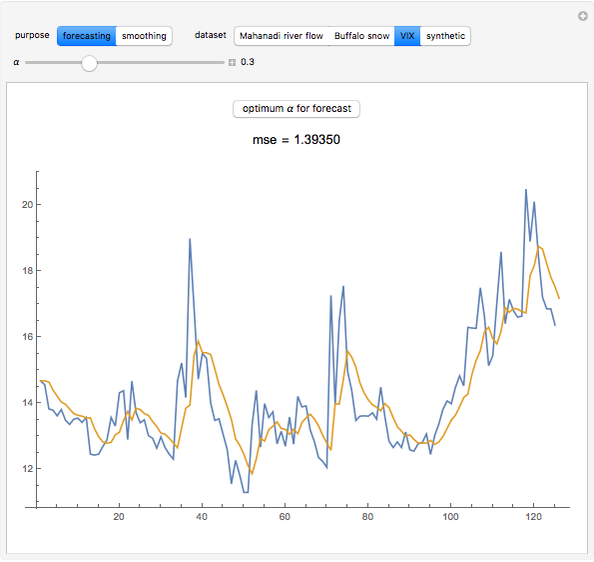

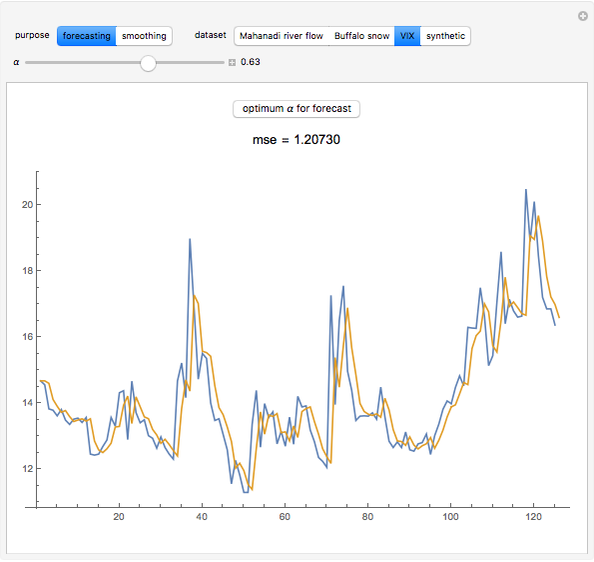

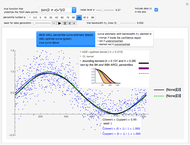

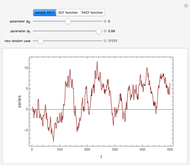

For stationary or nearly stationary data, the exponential moving average is a simple method for time-series forecasting. Choose between forecasting and smoothing to see the difference between them;  is the smoothing parameter in the exponential moving average and

is the smoothing parameter in the exponential moving average and  is the mean square error between the forecast (red curve) and actual values of the data (blue curve). Larger values of cause less smoothing.

is the mean square error between the forecast (red curve) and actual values of the data (blue curve). Larger values of cause less smoothing.

Contributed by: Bruce Atwood and Lingzhi Meng (August 2013)

(Beloit College)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The forecast at time  is given by

is given by  where

where  is the actual value of the time series at time

is the actual value of the time series at time  . This recursion starts at

. This recursion starts at  . When

. When  , the forecast is

, the forecast is  for all time and when

for all time and when  , the forecast is the last observation. For more information on forecasting with exponential smoothing methods, see [1].

, the forecast is the last observation. For more information on forecasting with exponential smoothing methods, see [1].

Students should ask themselves: is there any relationship between the appearance of the data and the optimum value of for forecasting? Why isn't the exponential moving average a very good forecasting method for data with a trend?

Reference

[1] S. G. Makridakis, S. C. Wheelwright, and R. J. Hyndman, Forecasting, Methods and Applications, 3rd ed., Hoboken, NJ: John Wiley & Sons, Inc., 1998.

Permanent Citation

Extreme Value Forecasting

Extreme Value Forecasting

Marshall Bradley Data Smoothing

Data Smoothing

Jon McLoone Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber Aliasing in Time Series Analysis

Aliasing in Time Series Analysis

Ian McLeod Nonparametric Regression and Kernel Smoothing: Confidence Regions for the L2-Optimal Curve Estimate

Nonparametric Regression and Kernel Smoothing: Confidence Regions for the L2-Optimal Curve Estimate

Didier A. Girard Autocorrelation and Partial Autocorrelation Functions of AR(1) Process

Autocorrelation and Partial Autocorrelation Functions of AR(1) Process

Jozef Barunik Records in Sequences of Random Variables

Records in Sequences of Random Variables

Heikki Ruskeepää Stock Forecasting

Stock Forecasting

Andrew Tao Linear Regression

Linear Regression

Mikel Landajuela Nonparametric Additive Modeling by Smoothing Splines: Robust Unbiased-Risk-Estimate Selector and a Nonisotropic-Smoothing Improvement

Nonparametric Additive Modeling by Smoothing Splines: Robust Unbiased-Risk-Estimate Selector and a Nonisotropic-Smoothing Improvement

Didier A. Girard